As a homeowner, you are probably inundated with offers to refinance your current mortgage. Like most of us, you usually just discard those mass mailings along with all of the other credit card and junk mail offers.

But have you ever wondered if you should refinance your home?

Just like buying a home, refinancing can be a daunting and confusing process. However, refinancing at the right time and with the right terms could save you thousands of dollars in the long run. On the other hand, an ill-advised refinance could tack on years to your current mortgage and cost you thousands in out of pocket expenses.

Think about it this way, mortgage lenders are not in the business of saving you money. They are for-profit entities and the system is designed for them to become profitable–not you. These companies spend thousands on advertising and understand the market and this process far better than the average consumer. Before you take the plunge, ensure you’ve done your due diligence.

Do the Math

Prior to contacting a lender and diving head-first into this process, do a little research. Find out what the average Annual Percentage Rate (APR) for home mortgages and mortgage refinancing is. The APR is the interest charged for borrowing money –or the cost of the loan. For mortgage loans, excluding home equity lines of credit, it includes the interest rate plus other charges or fees. For home equity credit lines, the APR is just the interest rate.

| Product | APR | |

| Conforming and Government Loans | ||

| 30-Year Fixed Rate | 4.538% | |

| 30-Year Fixed-Rate FHA | 5.552% | |

| 30-Year Fixed-Rate VA | 4.546% | |

| 15-Year Fixed Rate | 3.852% | |

| 7/1 ARM | 4.064% | |

| 5/1 ARM | 4.047% | |

| 5/1 ARM VA | 3.486% | |

| Jumbo Loans—Amounts that exceed conforming loan limits | ||

| 30-Year Fixed-Rate Jumbo | 4.381% | |

| 15-Year Fixed-Rate Jumbo | 4.152% | |

| 7/1 ARM Jumbo | 3.953% | |

**Rates, terms, and fees as of 3/10/2017 and are subject to change without notice.

How does your current interest rate compare? If your APR will not be reduced by at least a full percentage point, refinancing is not going to be beneficial for you—unless you are seeking to move from an adjustable rate mortgage (ARM) to a fixed-rate.

Now let’s do some quick math using a refinancing calculator:

Let’s say you purchased your home in 2007 and the original purchase price was $250,000 at an APR of 4.85 percent (fixed rate). Your refinance preapproval APR is 3.75 percent for a 30-year term and you currently owe $222,000 on your home. We will estimate closing costs to be $6,000 (which is the current average).

You simply plug those numbers into the calculator and instantly you have a fairly accurate gauge to help you determine if refinancing is a good idea and how long it would take for you to actually begin seeing the savings.

According to this example, you would save just over $40,000 dollars over the lifetime of this loan. However, it would take approximately 2 years for you to break even and recoup all of the closing costs.

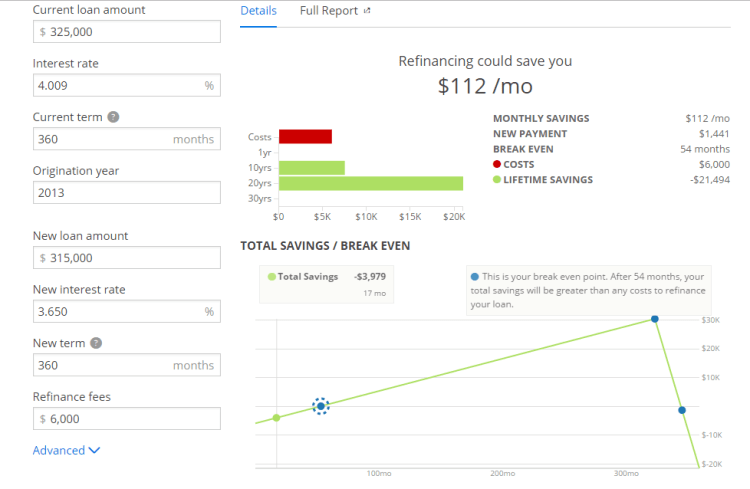

Let’s look at another example:

The original cost of your home purchased in 2013 is $325,000 at an APR of 4.009 percent (fixed). The refinance loan amount is $315,000 at an APR of 3.65 percent for a term of 360 months (30 years) with $6,000 in closing costs.

In this example, your total savings over the life of the loan is $21,494 but it is going to take you 54 months—nearly five years just to break even. Add to that the fact that you have already made plans to sell within the next five to seven years. In this case, even though you will save money long term and your monthly payments would be lowered, refinancing may not be the best financial option for you.

Calculate Your Home’s Loan to Value Ratio

You have to have enough equity in your home in order to refinance which is determined through an appraisal of the home. You qualify for refinancing based on your property’s loan to value ratio (LTV). This is calculated by comparing the current market value of your home to what you owe. An 80 percent LTV is considered the magic number and is necessary for refinancing. Unfortunately, you must actually submit the refinance loan application and pay the associated fees—which could be hundreds of dollars– in order to determine if you are even eligible to refinance your home. Here are a few things that can help you estimate your LTV:

- Property tax valuations

- Recent sales of comparable properties

- News reports about local home prices

- Sightings of for sale and foreclosure signs on nearby homes

- Estimates from local real estate brokers or appraisers

- Home valuation websites.

Other things to consider

Now that you have done the math and have an idea of your home’s LTV, let’s move on to some other things to consider before making the final decision concerning refinancing.

Here are some of the overall benefits of refinancing:

- Save money: Taking advantage of a lower interest rate will save you money long term. If you don’t plan to sell your home in the near future, this is an excellent option.

- Reduce monthly payments: The immediate benefit to refinancing is your overall monthly payments are lowered and you have more disposable income

- Move from an ARM to a fixed rate loan: This is one of the most popular reasons to refinance. Moving to a fixed rate mortgage with a low interest can save you money although that is not a guarantee. It can eliminate the hassle that an ARM can create after the initial period of the low fixed interest rate ends. ARMs adjust frequently—making budgeting more difficult as you never know exactly what your payment will be. Fixed rate mortgages remove the guess work.

- Change mortgage companies: Sometimes people are unhappy with their mortgage company or things may happen within the company that makes you feel uneasy (the company is sold or merges with another company, rumors of unethical business practices, etc.). Refinancing and moving to another mortgage company can resolve this issue.

- Secure a different more favorable loan: The terms of a loan can greatly affect the overall value of the loan. Moving from a conventional loan to a VA or even FHA could be very beneficial especially if your circumstances change (loss of a job or better refinancing terms—i.e. no closing costs, appraisal, etc.).

- Take equity out of the home: Refinancing your home to lower your interest rate and to borrow against the home’s equity is another reason many people refinance. Usually, the money is used for home improvements or to make other substantial purchases. The terms for refinancing under these conditions are a bit different and the interest rate is going to be higher.

Things you should know before refinancing:

- Understand that refinancing is not a second mortgage it is quite simply getting a new mortgage that replaces the original one. Refinancing is done to allow a borrower to obtain a better interest term and rate. The first loan is paid off, allowing the second loan to be created.

- Your credit score is very important. For borrowers with a perfect credit history, refinancing can be a good way to convert a variable loan rate to a fixed, and obtain a lower interest rate. For borrowers with less than perfect credit, bad credit, or too much debt, refinancing can be risky and even detrimental. The real danger in refinancing lies in ignorance. Without the right knowledge, refinancing can actually increase your interest rate instead of decreasing it.

- Refinancing can actually add years to your loan. If you have been paying on your home for 10 years and you refinance for a 30-year term—you’ve just added an additional 10 years to the loan. Bringing the total term for repayment to 40 years instead of30. You may want to consider refinancing for a shorter term such as 20 or 15 years. Your monthly payments will be a bit higher but you pay down the principle quicker which equates to less money going towards interest.

- Are you able to pay points to lower your interest rate? A point is a fee equal to 1% of the loan amount. You can pay this fee up front and lower your interest rate. Casey Fleming, author of “The Loan Guide: How to Get the Best Possible Mortgage” and a mortgage professional in the San Francisco Bay area believes it makes sense to pay for points if you can afford to.

“In most cases, it makes a lot of sense to pay money to bring down the interest rate. Paying three points, for example, could lower your interest rate from 4.25 percent to 3.5 percent. (Points are fees. One point is equal to 1 percent of the loan amount, so one point on a $200,000 loan would be $2,000.) Over years, that could shave way more than you paid in points off your balance. “It’s a huge difference, much, much larger than you would think,” Fleming says.

- There are fees. Refinancing a loan comes with all of the same fees that were paid when you first purchased the home. You remember them (this list is not exhaustive):

- Mortgage application fee

- Appraisal report

- Home inspection

- Loan origination fee

- Document preparation fee

- Flood certificate

- Title search

- Title insurance

- Recording fee

- Underwriting fee

- Attorney fees

These fees are usually bundled together and are labeled closing costs, which can be paid upfront or rolled into the loan (some FHA and VA loans do waive some of these fees). When financing companies advertise “no closing costs” what they mean is there are no upfront closing costs—you will pay them, the question is when?

- If you are considering refinancing as a way to borrow money against your equity, you may want to go with a conventional loan or a home equity line of credit. Casey Fleming puts it this way:

“If you take out $20,000 in cash on your 30-year mortgage to remodel your kitchen, you’re actually paying for that kitchen for 30 years. You may have to make some of those improvements two or three more times before you’re finished paying off the first round. You’re financing a paint job for 30 years.”

Bottom Line

When deciding if refinancing is a viable option for you, try to focus on the big picture. Consider the new loan’s term length and total interest; the break-even time, your overall plan for repayment, your credit history and financial situation and your long-term plan for your home. Refinancing can create substantial savings long term when done correctly but could be financially devastating if entered into ill-advised.